AFT Pharmaceuticals Limited (AFT.NZ) Maintains Bullish Trajectory Ahead of FY26 Results

AFT Pharmaceuticals Limited (AFT.NZ) is approaching a critical reporting milestone on May 21, 2026, as the organisation prepares to release its full-year financial results for the period ended March 31, 2026. The company enters this reporting cycle with significant operational momentum, underpinned by a 39.69% share price appreciation over the past 52 weeks and a strategic expansion into the United States market. With a current market capitalisation of NZ$383.811 million, the pharmaceutical specialist is navigating a high-growth phase, supported by record half-year revenues and a clear pathway toward a NZ$300 million annual revenue target by the end of the 2027 financial year.

Company Overview

AFT Pharmaceuticals Limited (AFT.NZ) operates as a multinational specialty pharmaceutical entity based in New Zealand. The organisation distinguishes itself through an asset-light business model that prioritises the development, licensing, and marketing of branded pharmaceutical products over heavy manufacturing infrastructure. This strategic positioning allows the company to focus capital on regulatory approvals and global distribution across over-the-counter (OTC), prescription, and hospital channels. The product portfolio is diversified across several therapeutic categories, including pain relief, eye care, and infection treatment, providing a broad revenue base that spans multiple international jurisdictions.

By building value around product selection and intellectual property rather than physical production plants, the company maintains a flexible cost structure. This model has enabled the firm to scale its operations from its New Zealand headquarters into a global presence, leveraging partnerships to enter complex markets such as the United States and Europe. The focus remains on high-value branded products where regulatory barriers to entry provide a competitive moat.

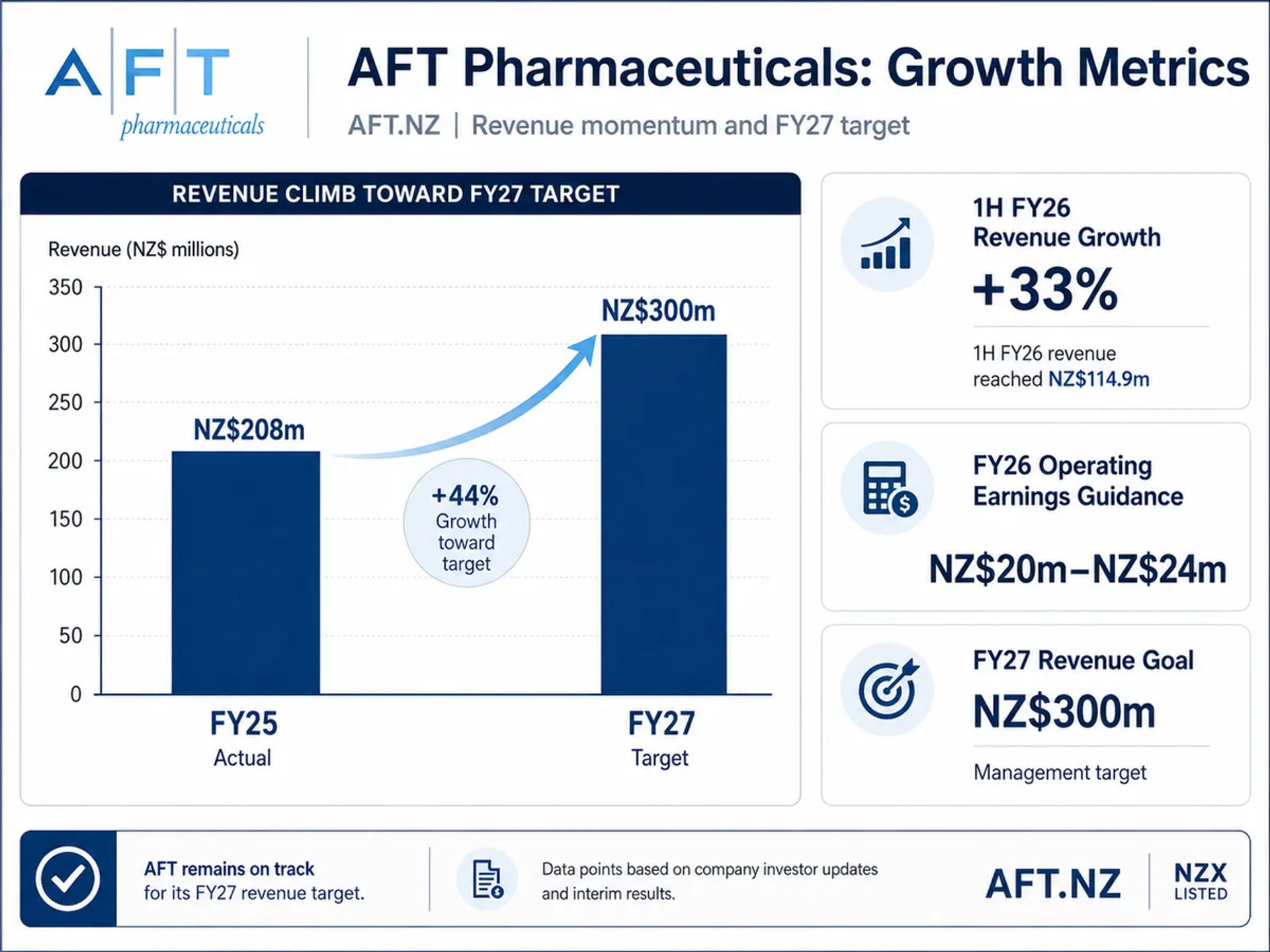

Financial Metrics

The financial performance of AFT Pharmaceuticals Limited (AFT.NZ) has shown robust growth through the 2025 and 2026 fiscal periods. For the full year ended March 31, 2025 (FY25), the company reported total revenues of NZ$208 million. This resulted in a normalised operating margin of 8.5% and a normalised profit before tax of NZ$17.7 million. Shareholders received a dividend of NZ$0.0180 per share for the FY25 period, reflecting a trailing dividend yield of approximately 0.49% based on the current share price of NZ$3.66.

Growth accelerated significantly in the first half of the 2026 financial year. For the six months ended September 30, 2025, the company achieved record revenue of NZ$114.9 million, representing a 33% increase compared to the prior corresponding period. This revenue surge facilitated a return to profitability at the operating level, with an operating profit of NZ$4.7 million reversing a NZ$1.8 million loss from the first half of FY25. Net profit after tax for the half-year stood at NZ$2.7 million.

Valuation metrics currently reflect the market's growth expectations. With a trailing earnings per share (EPS) of NZ$0.1247, the stock trades at a price-to-earnings (P/E) ratio of approximately 29.35x. The balance sheet shows a net debt position of NZ$20.9 million as of September 30, 2025. Management has provided operating earnings guidance for the full FY26 year between NZ$20 million and NZ$24 million, while reiterating the long-term objective of reaching NZ$300 million in annual revenue by FY27.

Recent Catalysts

A primary driver of recent sentiment for AFT Pharmaceuticals Limited (AFT.NZ) is the strategic partnership with Cost Plus, the United States-based pharmacy chain. This agreement facilitates the distribution of Maxigesic® Rapid tablets across the US market, providing a significant entry point into the world's largest pharmaceutical economy. This partnership is expected to be a major contributor to the company's goal of sustained double-digit sales growth across all international markets.

In addition to the US expansion, the company has reported positive progress in its research and development pipeline. Successful engagements with the United States Food and Drug Administration (FDA) regarding a novel injectable iron treatment project indicate a maturing pipeline of high-value clinical assets. These regulatory advancements are critical for the company's long-term valuation, as they de-risk future revenue streams in the hospital and prescription sectors. The upcoming investor webinar on May 21, 2026, is expected to provide further clarity on the commercial rollout of these products and the performance of the Maxigesic® range in the North American market.

Technical Analysis

The technical profile for AFT Pharmaceuticals Limited (AFT.NZ) remains decidedly bullish as the stock trades near its 52-week highs. At the current price of NZ$3.66, the stock is positioned well above its key moving averages, indicating sustained upward momentum. The 50-day SMA currently sits at 3.52, while the 200-day SMA is at 3.26. The fact that the shorter-term average remains above the long-term average, and the price remains above both, confirms a primary uptrend.

Short-term momentum is also positive, with the 20-day EMA recorded at 3.56. The RSI (14) is currently at 64.66, which is classified as a neutral signal. While the RSI is approaching the overbought threshold of 70, it currently suggests there is still room for price appreciation before the stock becomes technically extended.

Furthermore, the MACD indicator is currently in a bullish configuration, with the MACD line trending above the signal line. This suggests that the recent price increase of 1.12% over the past two weeks is supported by positive momentum. The stock has successfully navigated a trading range between a 52-week low of NZ$2.51 and a high of NZ$3.80, with the current price sitting just 3.68% below its annual peak.

Analyst Sentiment

Market analysts maintain a positive outlook on AFT Pharmaceuticals Limited (AFT.NZ), with the consensus rating currently sitting at 'Buy'. This optimism is reflected in the average one-year price target of NZ$4.44, which implies a potential upside of approximately 21.3% from current levels. Analyst forecasts for the share price are relatively tight, ranging from a conservative low of NZ$4.24 to a high of NZ$4.72.

Recent shifts in sentiment have seen technical research firms upgrade the stock from a 'Sell' to a 'Hold' candidate as of May 7, 2026. While there have been historical revisions to earnings per share estimates, the prevailing view among the investment community is that the company's revenue growth trajectory and successful US market entry justify the current valuation premiums. The focus for analysts remains on the company's ability to convert its record revenues into expanded operating margins as it scales.

Risks and Outlook

While the growth prospects for AFT Pharmaceuticals Limited (AFT.NZ) are substantial, several risk factors warrant consideration. The company's net debt of NZ$20.9 million requires careful management, particularly as it continues to fund international expansion and R&D projects. Furthermore, the achievement of the NZ$300 million revenue target by FY27 relies heavily on the successful commercial execution of the Cost Plus partnership and the timely approval of new treatments by the FDA. Any regulatory delays or slower-than-expected uptake in the US market could impact the company's ability to meet its FY26 operating earnings guidance of NZ$20 million to NZ$24 million.

However, the outlook remains constructive. The company has demonstrated a consistent ability to grow sales across all markets, as evidenced by the 33% revenue increase in the most recent half-year period. The transition from a loss-making first half in FY25 to a profitable first half in FY26 suggests that the organisation is reaching an inflection point where economies of scale are beginning to manifest in the bottom line.

AFT Pharmaceuticals Limited (AFT.NZ) continues to demonstrate the efficacy of its asset-light, brand-focused strategy. With the share price trading at NZ$3.66 and maintaining a bullish technical posture above the 200-day SMA of 3.26, the market appears to be pricing in continued success for the organisation's global expansion. The upcoming full-year results on May 21 will be the next major catalyst to determine if the company can maintain its double-digit growth rate and progress toward its ambitious FY27 revenue objectives.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.