New Zealand housing market faces renewed price pressure as sentiment weakens

New Zealand's residential property market is navigating a period of heightened uncertainty, with several indicators suggesting a further slide in valuations through the remainder of 2026. While property consultancy Cotality data indicates a marginal 0.1% increase in house prices between March and April 2026, the annual trend remains negative, with prices 0.8% lower than in April of the previous year. This modest monthly pick-up has done little to offset a broader shift in market expectations, as economists and market participants prepare for continued volatility.

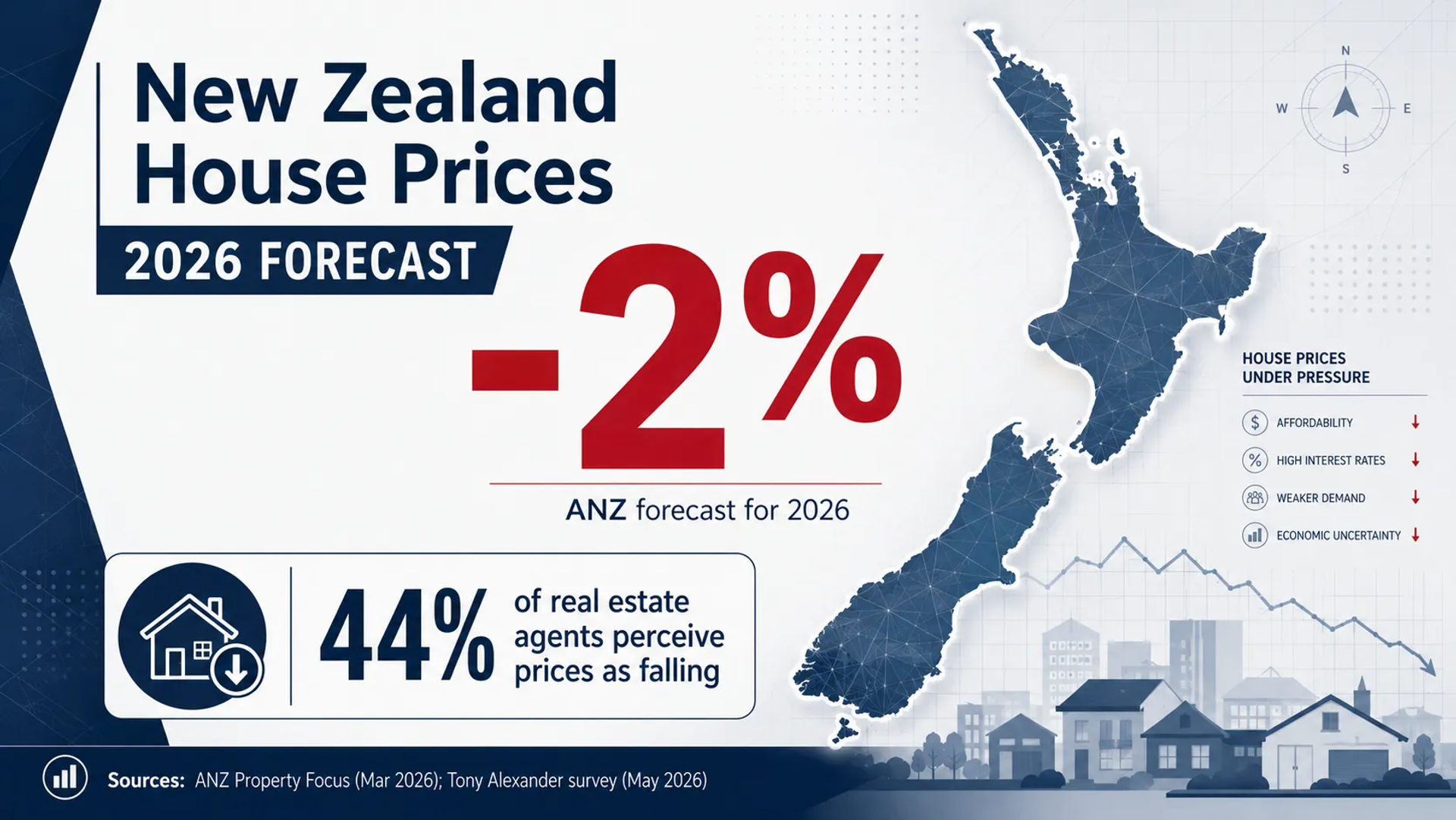

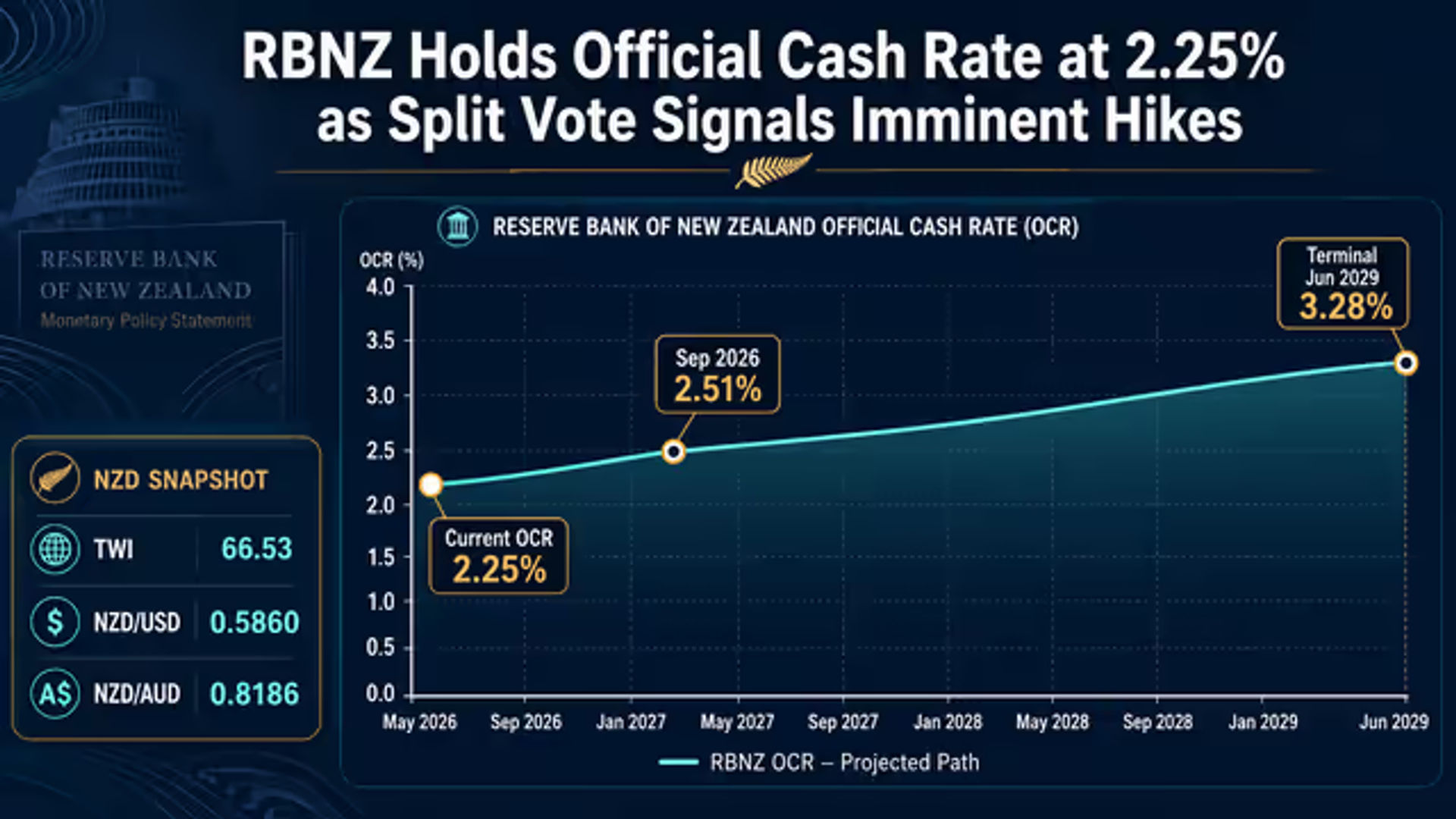

The Reserve Bank of New Zealand Financial Stability Report, published on May 5, 2026, indicates that housing-related risks are currently contained, though the market has remained broadly flat for the last three years. However, the report cautioned that rising mortgage rates present a risk of additional price reductions. This assessment aligns with revised projections from ANZ, where economists now expect New Zealand house prices to decrease by 2% over the course of 2026. Major institutions including Westpac, ASB, and BNZ have also adjusted their projections to reflect a flatter or declining price environment.

Market Sentiment and Buyer Activity

Sentiment among real estate professionals has reached its lowest point in several years. A survey of real estate agents conducted by Tony Alexander in May 2026 shows that 44% of agents perceive prices as currently falling, the most pessimistic reading since 2022. This lack of confidence is reflected in buyer activity, with a net 51% of agents noting a decline in open home attendance. These figures represent the weakest engagement levels seen in the market since early 2022, suggesting a significant cooling in demand despite the slight monthly price movement recorded by Cotality.

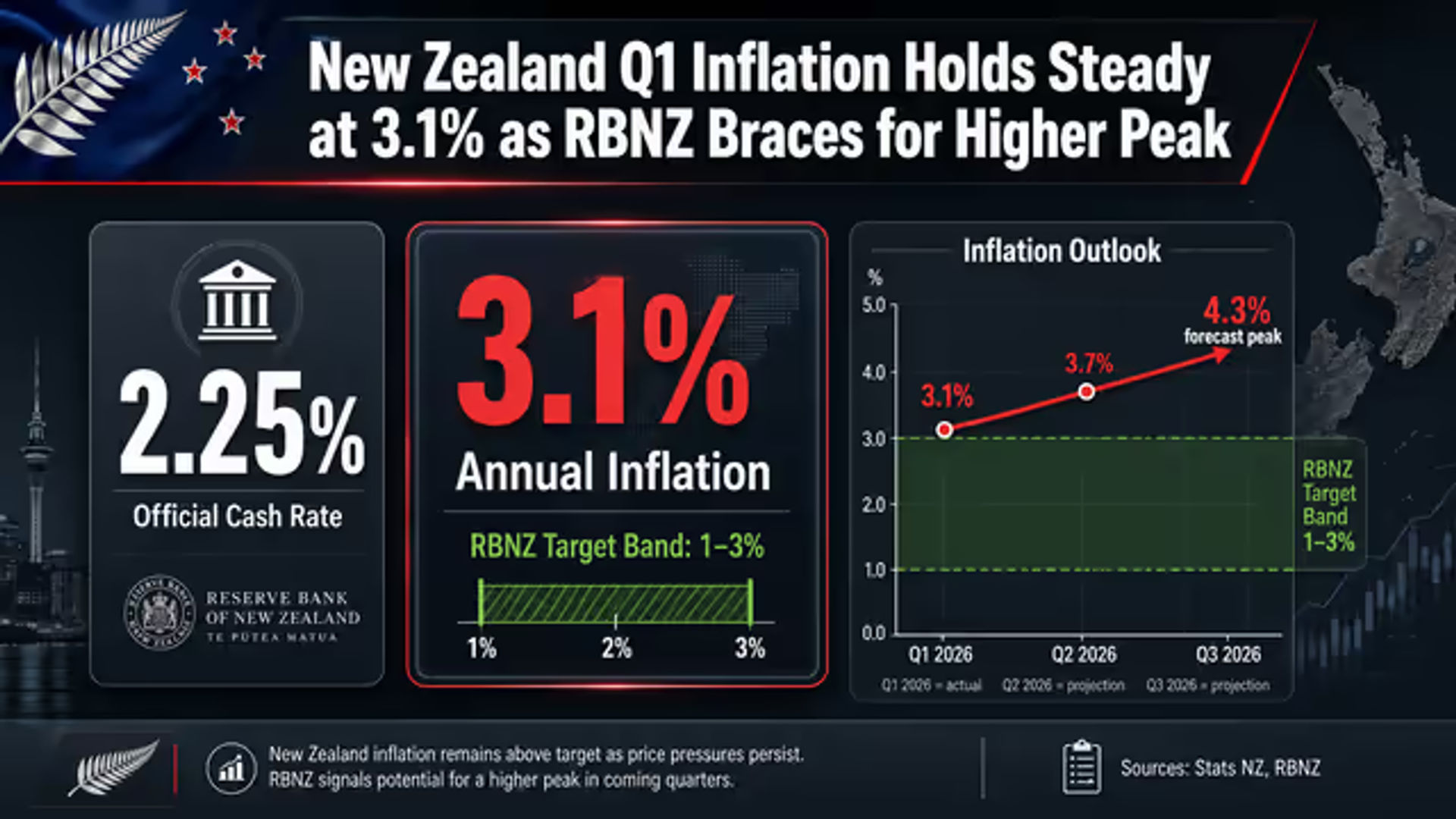

Household sentiment is also under significant strain. The ANZ-Roy Morgan Consumer Confidence Index for April 2026 fell by 11 points to 80.3, marking its lowest level in approximately three years. This decline in confidence is occurring alongside rising inflationary concerns. Two-year-ahead CPI inflation expectations rose by 0.9 percentage points to reach 6.6% in April 2026. These figures suggest that households are bracing for a prolonged period of high costs, which may further limit their capacity to service debt or enter the property market.

Supply Dynamics and Construction Pipeline

The supply side of the market continues to show resilience, potentially adding to the downward pressure on prices. Stats NZ figures for March 2026 show that seasonally adjusted new dwelling consents declined by 1.3%, but the annual pipeline remains robust. For the year ended March 2026, there were 37,813 new dwelling units consented, representing an 11% increase from the previous year. This healthy construction pipeline ensures a steady flow of new stock into a market where demand is already softening. A new transitional building consent system is also expected to become operational by mid-2026, which may further influence supply dynamics.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.