Auckland Property Values Slip in April as National Market Records Third Monthly Gain

Auckland’s residential property market diverged from the national trend in April 2026, with median values recording a slight decline despite a third consecutive month of modest growth across New Zealand. According to the latest Home Value Index from Cotality NZ, Auckland’s median house price slipped by 0.1% in April to reach just over $1.04 million.

In contrast, the national median residential property value rose by 0.1% over the same period, reaching $809,101. While the national market shows signs of a fragile recovery, Auckland remains under significant pressure, with property values now 3% lower than they were one year ago and 22.9% below the post-pandemic peak recorded in January 2022.

A Two-Speed Market Emerges

The April data highlights a growing disparity between New Zealand’s largest city and the rest of the country. While the national market has seen three consecutive months of incremental gains, the major urban centres of Auckland and Wellington both recorded 0.1% declines in April.

Within the Auckland region, the results were mixed. Data cited by the NZ Herald indicates that while sub-regions such as Papakura and North Shore saw small gains, these were offset by declines in Franklin, Auckland City, and Waitākere. This volatility follows a surprisingly strong March, where Barfoot & Thompson reported a median Auckland price of $1,030,000—a 13.9% increase from February—driven by a 60.8% month-on-month surge in sales volumes. However, the April figures suggest that the March momentum may have been a temporary spike rather than the start of a sustained recovery.

Inventory and Buyer Leverage

Despite the slight cooling in prices, inventory levels in Auckland remain elevated, continuing to provide buyers with significant choice. Opes Partners reports that Auckland’s housing inventory stood at 28 weeks in April 2026. While this is a slight decrease from the 29 weeks recorded in January 2026, stock levels remain above the long-term median.

Real Estate Institute of New Zealand (REINZ) data from earlier in the year noted that national inventory recently reached an 11-year high. For Auckland buyers, this environment of high stock and stagnant price growth maintains a market dynamic that favours purchasers, even as borrowing costs remain a primary concern.

Monetary Policy and Economic Headwinds

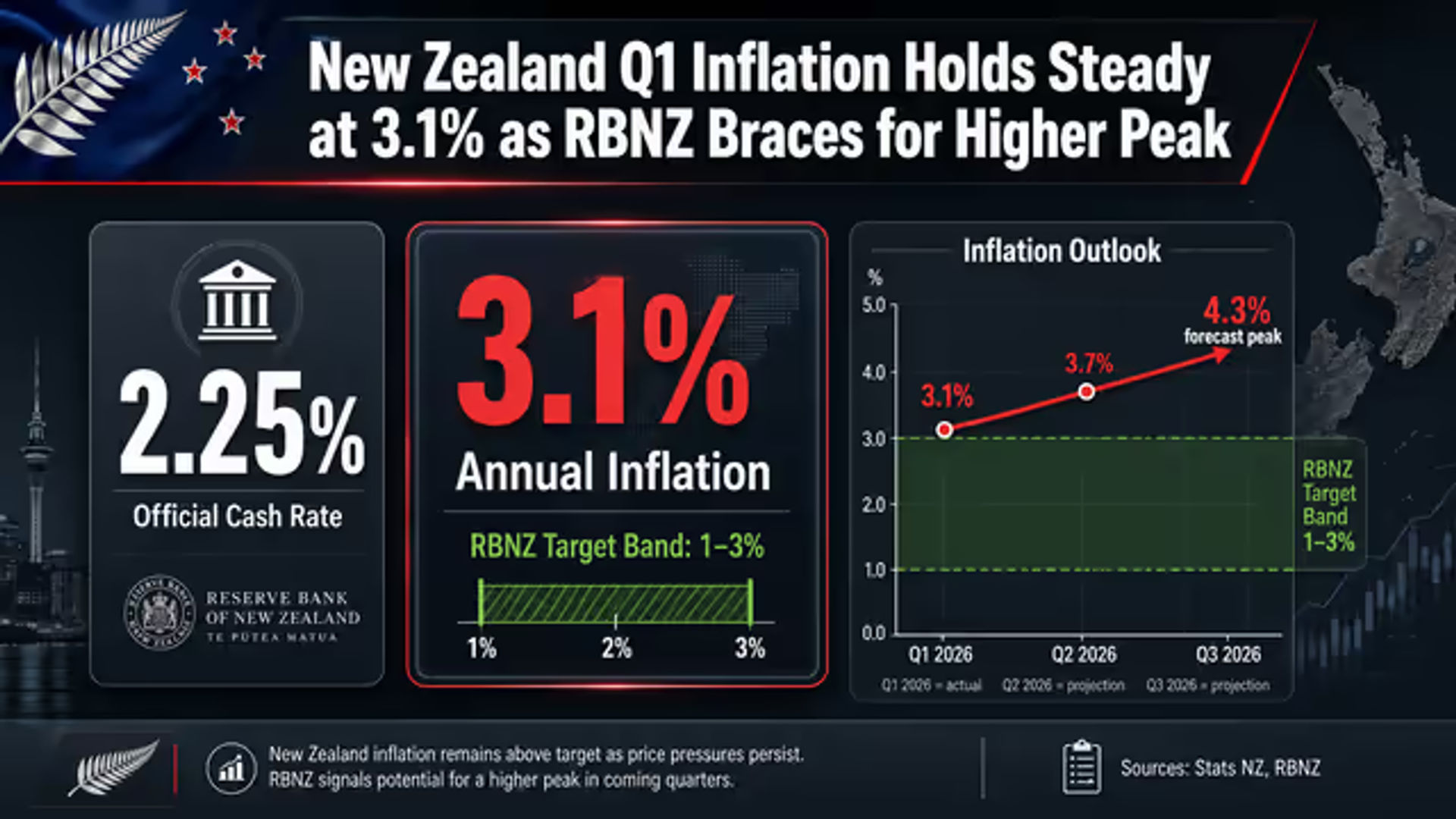

The Reserve Bank of New Zealand (RBNZ) maintained the Official Cash Rate (OCR) at 2.25% during its April 2026 meeting. However, the central bank signaled a hawkish stance toward persistent inflationary pressures. ANZ economists currently forecast that the RBNZ will begin a new cycle of tightening in July 2026, predicting three OCR hikes that would bring the rate to 3% by the end of the year.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.