Westpac Reports Solid Half-Year Profit and Maintains Dividend Amid Economic Headwinds

Westpac Banking Corporation has reported a statutory net profit of A$3.4 billion for the half-year ended 31 March 2026, demonstrating resilience despite a shifting economic landscape. The bank announced its results on 5 May 2026, maintaining an interim ordinary dividend of A$0.77 per share, which is fully franked. This decision is underpinned by a robust capital position, with the Common Equity Tier 1 (CET1) capital ratio reaching 12.4%, significantly exceeding the internal target of 11.25%. The dividend payout ratio for the period stands at 77.1% on a statutory net profit basis.

The financial results reflect a period of significant activity across the bank's core lending portfolios. Australian mortgages, excluding the RAMS brand, grew at 1.2x system during the half-year. This expansion contributed to total loans reaching A$890.3 billion, while customer deposits grew to A$745.2 billion. Business lending was a particular area of strength, recording a 16% increase over the year. These figures indicate sustained demand for credit through the first quarter of the year, even as the broader economy navigated rising interest rates and global geopolitical uncertainties.

Credit Quality and Risk Management

Despite the pressures of inflation and higher borrowing costs, Westpac observed an improvement in several key credit quality metrics. Stressed exposures as a percentage of total committed exposure decreased to 1.16%, representing a decline of 12 basis points from September 2025 and 20 basis points from March 2025. This downward trend suggests that a significant portion of the bank's portfolio remains resilient in the face of tighter monetary conditions.

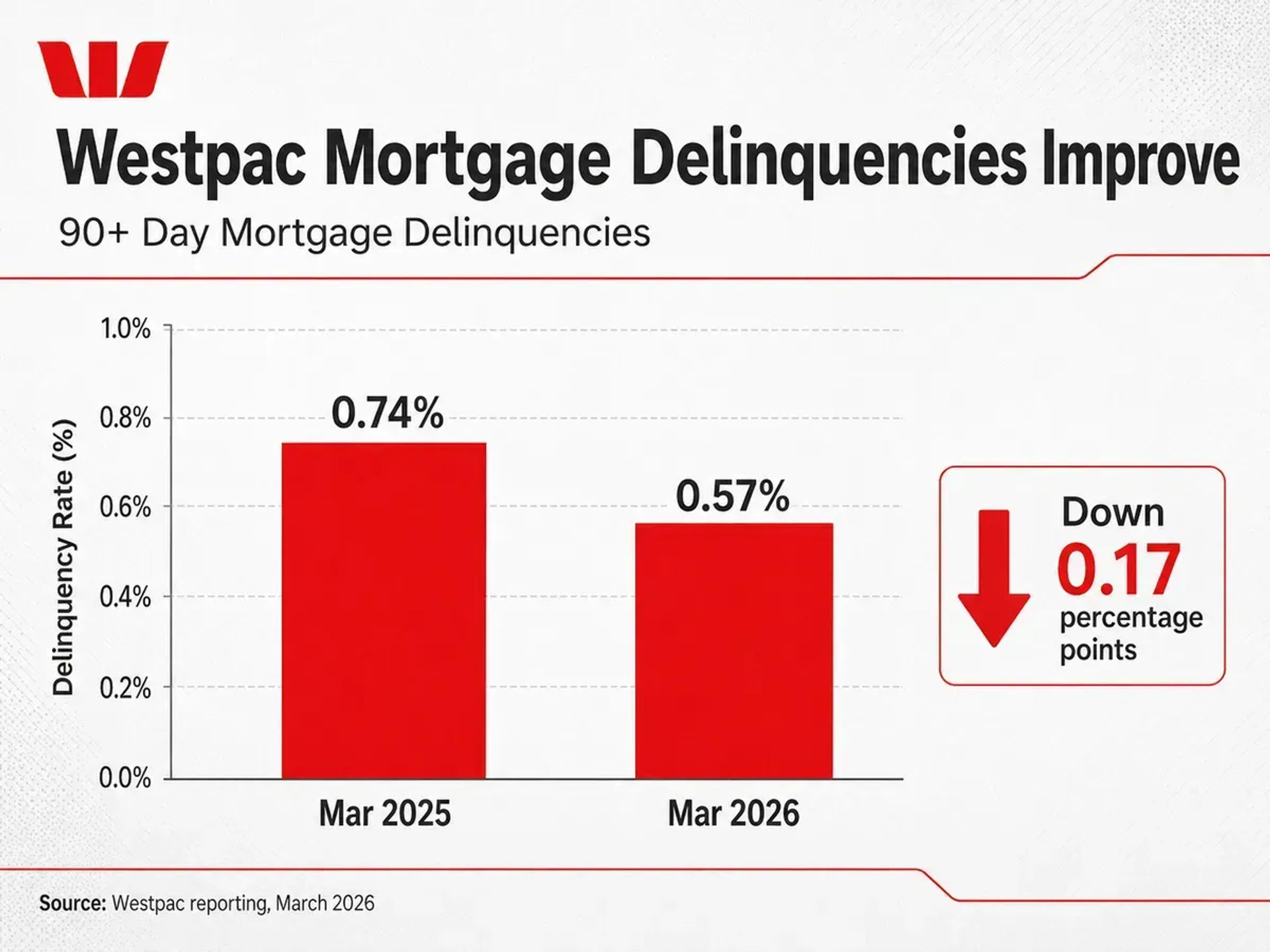

Household financial health also showed signs of stability during the reporting period. The rate of 90+ day mortgage delinquencies fell to 0.57%, a notable reduction from the 0.74% recorded in March 2025. This improvement in arrears occurred alongside the bank's efforts to manage its balance sheet prudently. However, the bank has maintained a cautious stance by increasing its provisions in response to a revised economic outlook and potential pressures on energy-intensive sectors, particularly as global unrest continues to impact supply chains and inflation.

Impact of Monetary Policy and Market Easing

The operating environment for Westpac has been increasingly influenced by the Reserve Bank of Australia (RBA) and its approach to managing inflation. A cycle of rising interest rates commenced in February 2026, which has begun to alter the trajectory of the housing market. While the half-year results to 31 March 2026 captured a period of strong lending growth, more recent data indicates a shift in momentum.

Mortgage applications eased in April 2026, following the commencement of the rate hike cycle. This slowing in home lending growth suggests that the cumulative impact of higher interest rates is beginning to manifest in consumer behaviour. The Reserve Bank of Australia (RBA) delivered a third rate hike for the year around the time of the bank's results announcement on 5 May 2026, citing global instability and persistent inflation risks as primary drivers for the policy tightening. This environment has also led to net interest margin compression as the bank navigates intense competition for deposits and higher wholesale funding costs.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.