Financial Markets Anticipate RBNZ Rate Hikes Amid Divergent Economic Forecasts

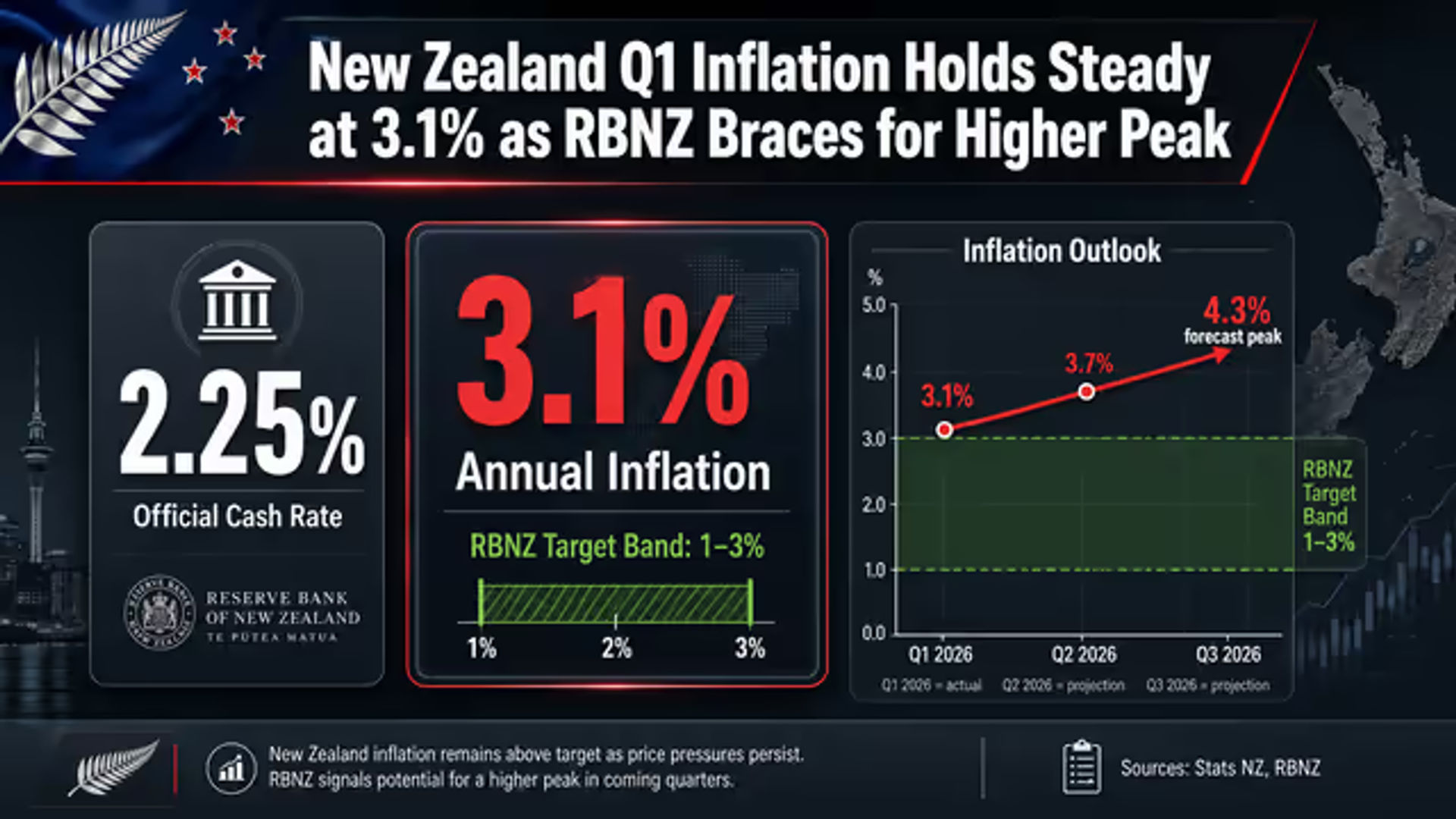

New Zealand financial markets are currently pricing in several 25 basis point increases to the Official Cash Rate over the coming year, reflecting a significant shift in sentiment regarding the domestic interest rate trajectory. This market positioning follows persistent global inflation concerns and recent monetary policy tightening by the Reserve Bank of Australia, which raised its cash rate to 4.35% on May 5, 2026. While the Reserve Bank of New Zealand maintained the Official Cash Rate at 2.25% during its meeting on April 8, 2026, the outlook for borrowing costs has become increasingly complex as domestic inflation remains outside the target range.

The annual inflation rate in New Zealand was 3.10% in the first quarter of 2026, a figure that remained unchanged from the final quarter of 2025. This level of price growth continues to exceed the Reserve Bank of New Zealand inflation target range of 1-3%, creating a challenging environment for policy setters. Compounding these domestic pressures are heightened consumer inflation expectations, which reached 6.6% in April. The central bank has already acknowledged that the conflict in the Middle East has altered the economic landscape, introducing risks of higher near-term inflation and a potentially weaker recovery for the national economy.

Divergent Forecasts Among Major Lenders

Economists at New Zealand's major commercial banks are currently divided on the timing and necessity of future rate increases. ANZ and ASB have both revised their projections, now forecasting that the Reserve Bank of New Zealand will begin raising the Official Cash Rate in July 2026. ANZ anticipates a series of three hikes starting mid-year, driven by the need to contain persistent inflationary risks. ASB similarly expects the tightening cycle to commence in July, noting that headline consumer price index inflation is projected to peak at 4.5% by the middle of 2026.

Westpac economists have provided a more specific timeline for policy adjustments, expecting 0.25% increases to the Official Cash Rate in September, October, and December of 2026. Under this scenario, the Official Cash Rate would reach 3.00% by the end of the year. This forecast is set against a backdrop of cooling economic activity, with Westpac projecting a GDP contraction of 0.4% for the second quarter of 2026. Furthermore, the labour market is expected to soften, with unemployment projected to peak at 5.6% by mid-2026. ANZ provides a slightly more pessimistic outlook for the labour sector, forecasting the unemployment rate to peak at 5.8% by the end of 2026.

The Case for a Cautious Approach

In contrast to the prevailing market sentiment and the forecasts of other major lenders, Kiwibank is advocating for a 'wait and see' approach. The organisation argues that zero immediate hikes are required, citing evidence of demand destruction within the domestic economy. On , reiterated its position that premature tightening could be detrimental, particularly as the economy faces a likely contraction during the second quarter of the year. This perspective highlights the existence of domestic economic spare capacity, which may eventually act as a natural brake on inflationary pressures without the need for further intervention.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.